Insurance has always been dependent on data. Anything from underwriting policies to processing claims is all about analyzing data to predict and reduce risk. By 2026, insurers could move from working on experimental projects to having generative AI algorithms that challenge the basic ideas of how insurers operate. The technology can draft customer communication, simulate fraud scenarios, and even come up with new products. It offers insurers new opportunities to serve their clients better and be more efficient.

Let’s talk about generative AI in insurance: how it can benefit and how companies can use it responsibly.

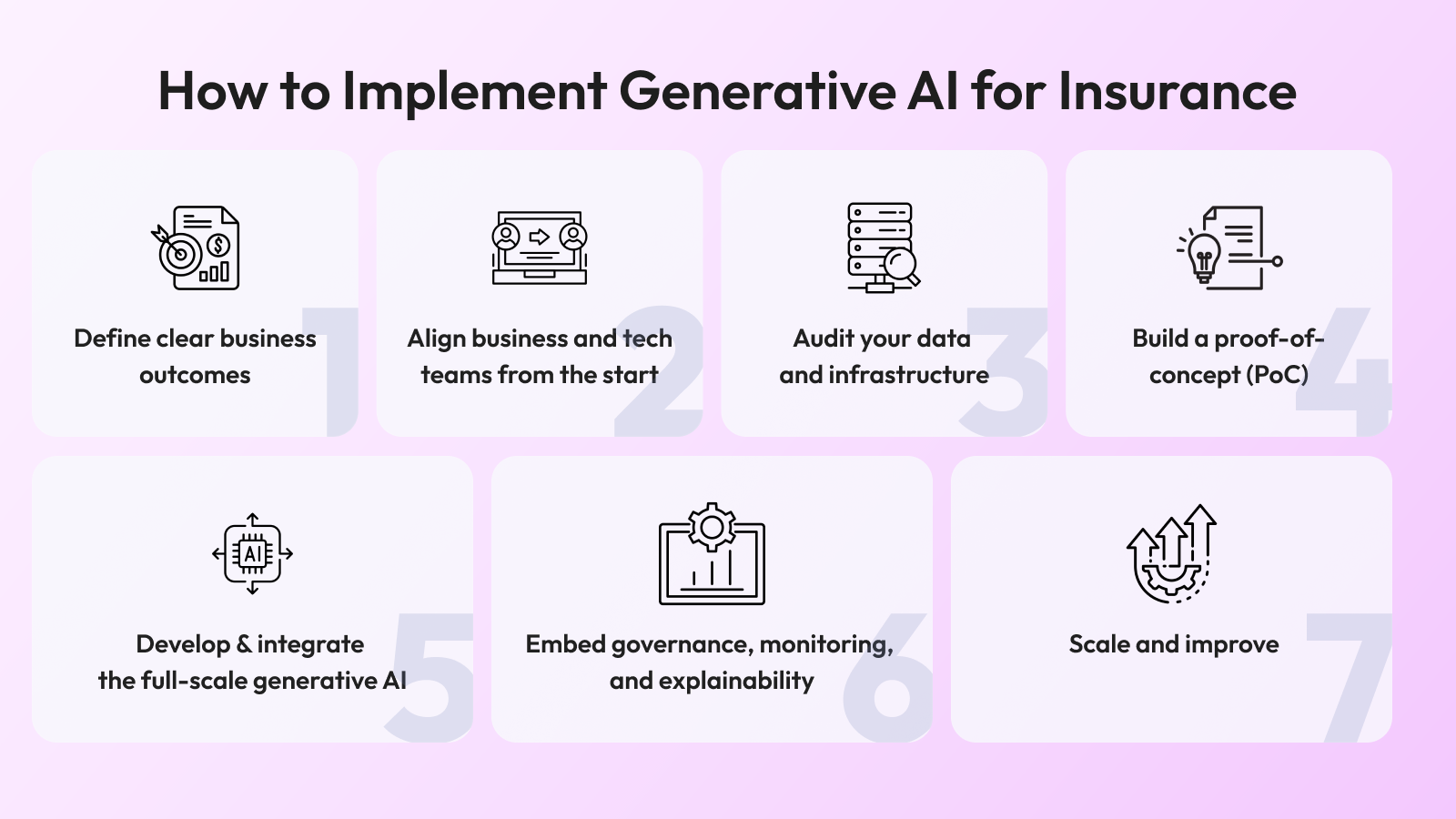

Top Generative AI Use Cases in Insurance

Generative AI has the power to change a slow, paper-oriented insurance system into an agile, insight-driven ecosystem. Insurers can automate complicated workflows, speed up the processing of claims, detect trends in fraud, and offer services to each policyholder. The technology can help underwriters and agents make quicker and data-based predictions, enhancing the client’s trust.

Insurers are rethinking their core operating models to unlock new levels of efficiency, speed, and personalization. According to McKinsey’s Global Insurance Report, the industry’s digital reinvention is accelerating as insurers seek scalable innovation levers.

What are the practical and highly significant generative AI use cases in insurance?

Policy recommendations personalized for the client

AI can look at a person’s lifestyle, financial situation, and risk factor to generate policy recommendations. Instead of receiving a list of insurance options, clients can get three to five policy choices that best suit them. It can be a mix of health, life, and home insurance tailored for a young mortgage family. It can lead to improved products and conversion.

Claims processing automation

The claims process is the most difficult bond between insurance companies and clients. It may eventually be one of the biggest pain points. While clients want transparent resolution as soon as possible, insurance companies want to avoid fraud and overhead.

Fraud detection and predictions

Insurers lose billions annually due to fraudsters. Simply generating potential fraud situations can help AI detection systems. Insurers can create lagging datasets that mimic fraudulent behavior to ensure that no customer information may be compromised. In other words, models are updated continuously as new fraud schemes are emerging, and they notice subtleties in behavior they might overlook.

Customer support and virtual assistants

No longer are chatbots themselves one-dimensional in which they respond with canned responses, generative AI has turned these into conversational assistant bots. They can handle complex queries, like telling consumers the coverage stipulations, assisting them in upgrading their insurance plan and even financial planning within an insurer’s products.

That means customers can have their questions answered immediately, instead of having to speak for 20 minutes in a contact center and getting responses that often sound scripted or lack empathy.

Product innovation and risk modeling

Insurers are able to simulate and trial new insurance products before taking them to the market, using generative AI. By combining app development insurance products with AI-based demand simulation and risk modeling, firms can iterate on offerings quicker and more easily.

For example, in climate change reporting, AI models could produce rich projections of devastating weather events. This allows insurers to assess risk and price policies that are both affordable for homeowners and profitable for providers in risky areas.

Benefits of Generative AI for Insurers

Generative AI is changing the way insurers are developing products, evaluating risks and serving customers. By automating processes and delivering actionable insights available from any data source, it enables insurance carriers to innovate at speed, reduce cost, and make better decisions throughout the value chain in underwriting, claims and customer experience.

Greater efficiency

Generative AI eliminates manual work in the insurance value chain. This accelerates the authorship of policy drafting, claims handling and other correspondence. Furthermore, GenAI lets employees to better use their time with more valuable tasks including customer management and business planning.

Improved customer experience

The ease of service businesses currently receive from tech companies represents what consumers in today’s marketplace also demand when it comes to their insurance. Trust is built by way of personalized engagements, swift issue resolutions and transparency. But with generative AI such experiences become available from insurers at scale.

Cost savings

The lower costs derive from decreased manual errors, faster claims adjudication and improved fraud identification. These savings could eventually be invested in superior products and pricing models to insurance companies.

Smarter decision-making

AI helps out leaders to make the decisions for risk exposure, pricing strategy and market opportunities by simulating scenarios and prognosticating outcomes. This proactive approach to business allows insurers to act when new trends emerge.

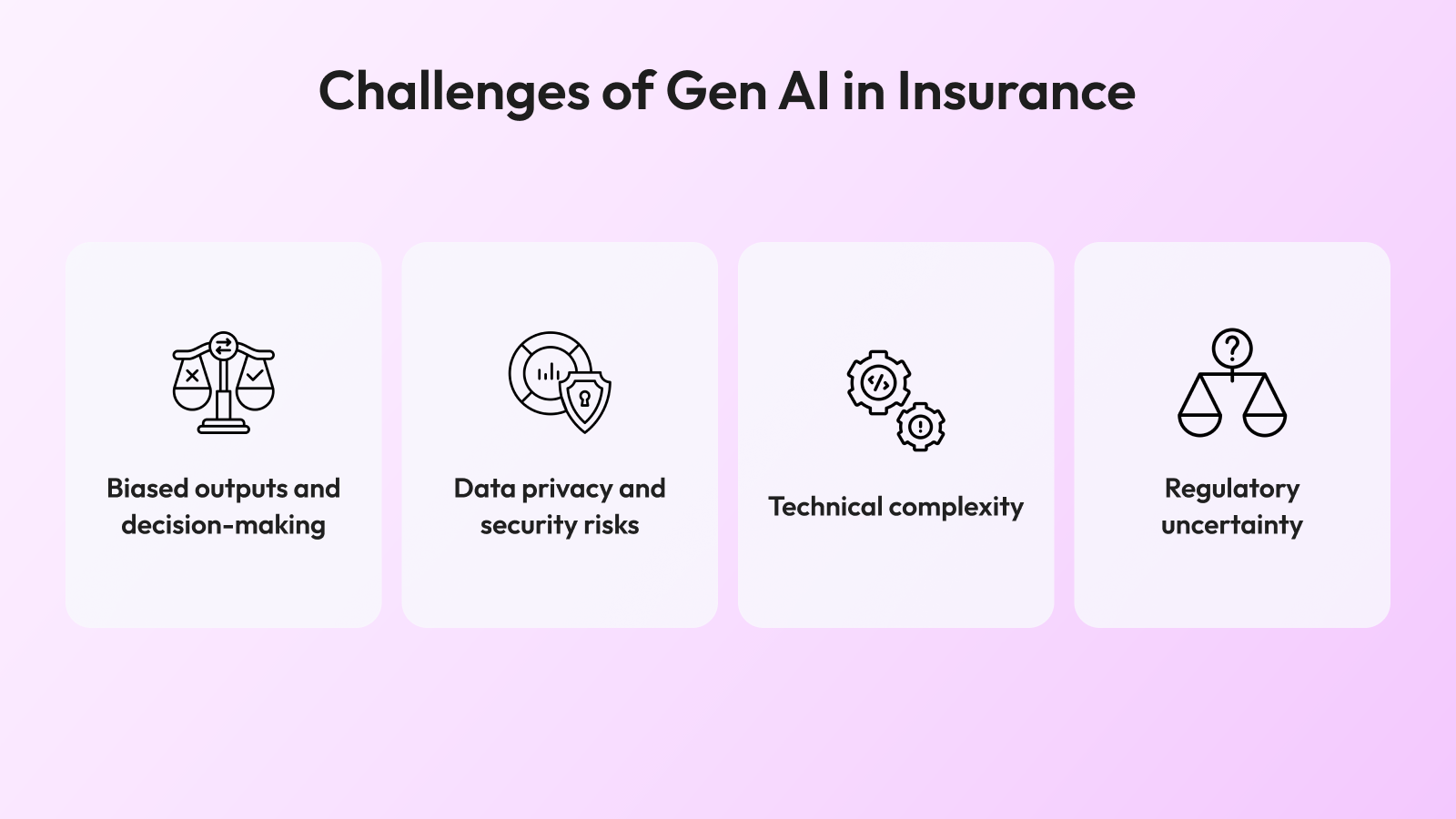

Challenges and Risks to Consider

Interesting as the opportunities may be, there are several challenges insurers must confront before they can fully lean in to generative AI.

Data privacy and security: Large gatherings of data are needed for AI models. So, it is still a case of providing a secure place for customer information where they can feel comfortable and secure knowing their data isn’t being protected fully and the business is compliant with the likes of GDPR.

Bias and fairness: AI recommendations can accidentally perpetuate discrimination, because of biases encoded in the historical data on which those systems were trained. They have to be audited regularly by very transparent processes.

The Road Ahead

So, here we are in 2026 and generative AI is an actual partner helping to reshape insurance and address the age-old puzzles of business. It allows businesses to serve customers better, run more efficiently and create new products for today’s risks. Whomever emerges winners in striking this balance, delivering both efficiency and empathy, will determine the next generation of insurance.